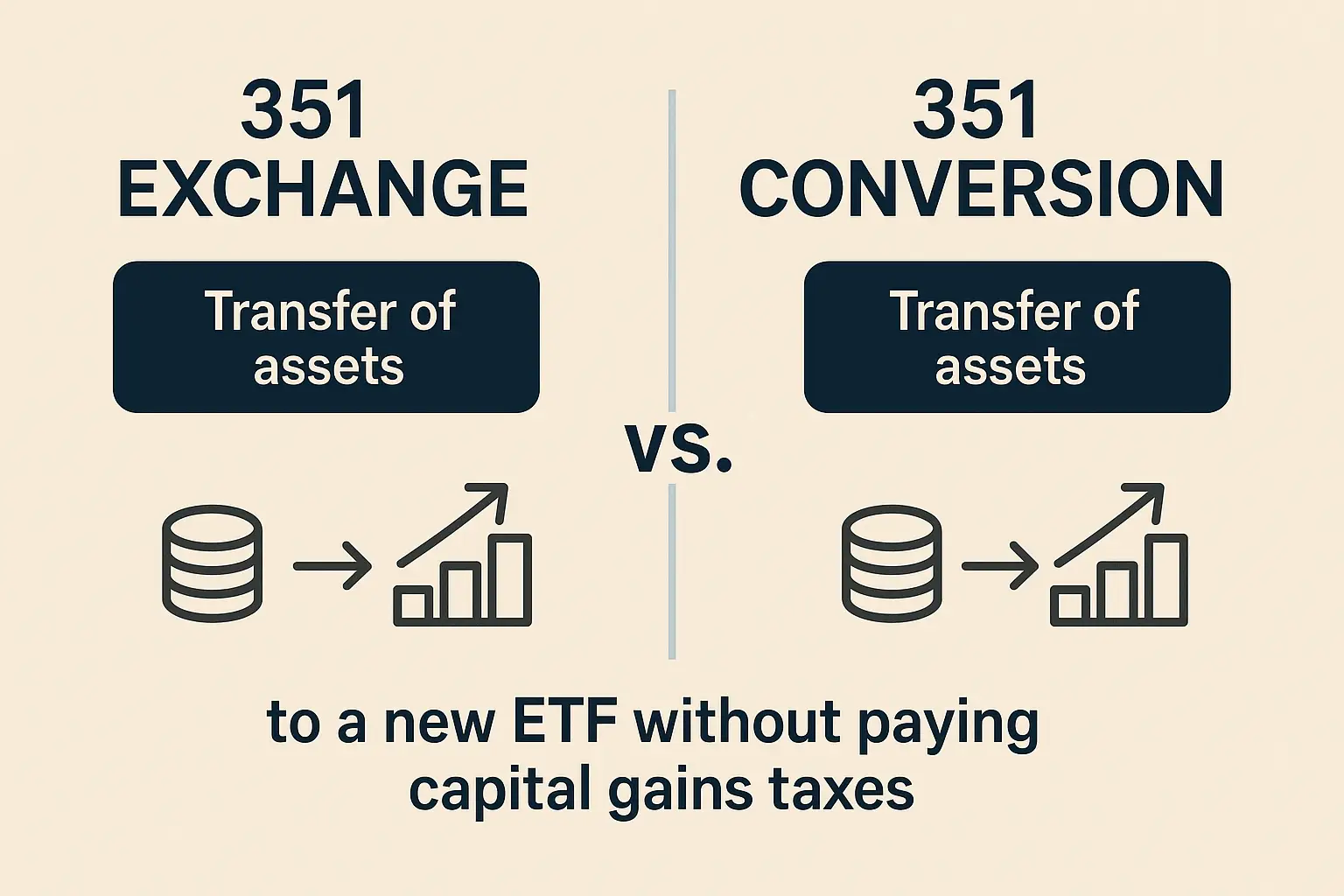

When discussing the strategic move of investment portfolios, such as Separately Managed Accounts (SMAs), into the efficient structure of an Exchange Traded Fund (ETF) without triggering immediate tax liabilities, you’ll often encounter two key phrases: 351 exchange and 351 conversion. You might wonder if these are different processes that commonly get confused like Exchange Fund and Exchange Traded Fund. Both “Section 351 exchange” and “Section 351 conversion” are correct to describe the process of transferring assets into an ETF under Section 351 of the U.S. Internal Revenue Code. Let’s delve into why both terms are applicable:

The Foundation: Section 351 of the Internal Revenue Code

A “Section 351” refers to a specific part of the tax code that allows for a tax-free transfer of property (like stocks and securities) to a corporation in exchange for stock in that corporation. This favorable tax treatment is granted as long as certain conditions are met, such as diversification requirements and the transferors maintaining control of the newly formed entity.

The “Exchange” Aspect: A Direct Swap of Assets for Shares

The fundamental mechanism of Section 351 is indeed an exchange. Investors transfer their assets directly to a newly formed corporation (in this case a new ETF), and in return, they receive shares of that corporation (ETF). This direct swap of property for stock is why the term “Section 351 exchange” is frequently used. It highlights the nature of the transaction as a direct exchange, similar in principle to tax-deferred exchanges in other areas like real estate (1031 exchange) or with insurance and annuities (1035 exchange). The focus here is on the tax-free nature of this exchange.

When “Conversion” Is Used: Transforming Investment Structures

When this “exchange” under Section 351 is applied specifically to move assets from one type of investment structure (like an SMA or a collection of individual holdings) into a different structure, an ETF, the term “conversion” becomes highly relevant. Phrases like “351 ETF conversion” or “SMA to ETF 351 Conversion” emphasize the transformation that is occurring. The existing portfolio is being converted into the ETF wrapper, offering benefits like enhanced liquidity, transparency, and potentially lower costs. The use of “conversion” underscores the change in the investment vehicle itself.

In Conclusion: Two Names For The Same Tax-Advantaged Process

Ultimately, the process of moving assets into an ETF under IRS Section 351 can be accurately described as both a 351 exchange and a 351 conversion.

- 351 exchange emphasizes the underlying tax-free transaction where assets are exchanged for stock in a newly formed corporation (the ETF).

- 351 conversion is used more with the transformation of an existing investment portfolio into the ETF structure.

Therefore, neither term is inherently more correct than the other. Instead, they represent different perspectives on the same tax-advantaged process. Whether you hear it referred to as a 351 exchange or a 351 conversion, the core concept remains the same: leveraging Section 351 of the Internal Revenue Code to move diversified portfolios into an ETF structure without triggering immediate capital gains taxes.